Introduction to SDR

The FCA’s ‘Sustainability Disclosure Requirements (SDR) and investment labels regime’ (PS 23/16) is a package of measures – introduced by the regulator in November 2023. The new rules are designed to improve transparency and trust in UK based retail funds that are promoted as having ‘sustainability’ (environmental and, or social) characteristics and strategies.

These rules were initially ‘socialised’ in November 2021 in the UK government’s ‘Sustainable Investing Roadmap’. Whilst SDR is now part of UK financial services regulation, the area continues to evolve, and SDR is expected to broaden in scope over time.

- Note: In April 2025 the FCA announced that plans to extend SDR to portfolios had been paused. In addition offshore funds are not yet in scope of the SDR regime. (Both remain expected – although timescales, requirements etc are unknown).

- FCA climate change and sustainable finance page

- Further information on good and bad practices was published by the FCA on 27 February 2026.

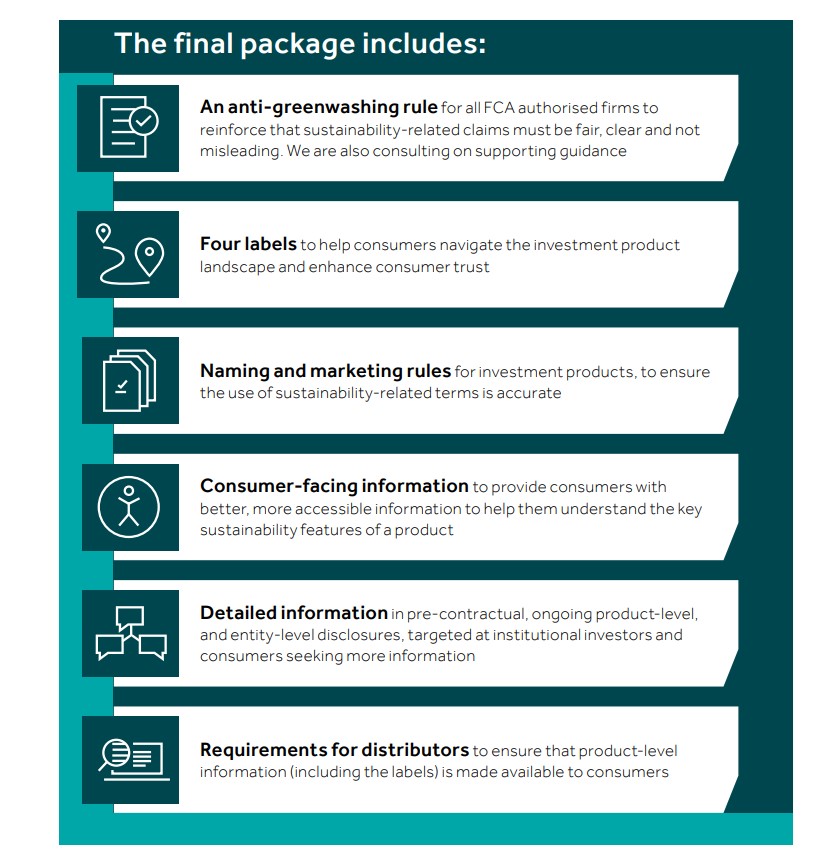

The following graphic, published in the FCA’s SDR document introduces its key elements:

Understanding SDR basics:

The following is our understanding of the key aspects of the rules. Please also see the FCA website.

- Note – Annex 2 of SDR provides a run through of the new rules in their entirety.

What is SDR?

SDR is a package of interconnected measures designed to ensure individual investors have access to reliable, decision-useful sustainability information when considering (in scope) investment funds.

SDR has a number of aims.

SDR refers to three core intended outcomes (see SDR PS23/16 figure 1), summarised as aiming to:

- Address greenwash, in order to protect clients

- Increased sustainability information – to protect markets

- To improve competition, by enabling consumers to find funds using sustainable fund labels

SDR comprises six topics:

- Anti greenwashing rule. The anti-greenwash rule requires any references to the sustainability characteristics to be consistent with the sustainability characteristics of the product or service and for communications to be ‘clear, fair and not misleading’. FG24/3 explains further – and includes examples, including reference to the need for references to be correct, clear, complete and able to be compared. See ‘Sustainability references should be:’ FCA image.

- Labels. From July 2024, in-scope funds that ‘intentionally’ focus on positive environmental and or social outcomes can choose to adopt one of four sustainability labels, subject to certain disclosure requirements. Broadly similar funds should indicate if they have chosen not to use a label (and meet certain rules).

- Naming and Marketing rules. Only funds that have adopted an SDR label can now have ‘sustainable’, ‘sustainability’ or ‘impact’ in their name. Similar terms (responsible, environmental etc) can be used, but must only be used to accurately describing alignment to fund activities – to guard against potentially misleading clients. This has led to many fund names being changed.

- Consumer facing information. Managers of labelled funds (and similar – which promote environmental and social characteristics) must publish a two-page ‘Consumer Facing Disclosure’ (CFDs) which has prescribed content. Unlabelled funds that are promoted as having significant environmental or social characteristics must also publish CFDs.

- Detailed information. Detailed pre-contractual sustainability information must be available – typically in a fund’s prospectus. Additional comprehensive fund and fund management entity level disclosures will also be required from late 2025 and 2026.

- Requirements for distributors. Distributors, such as platforms, are required to show which funds are labelled, with links to required information (CFDs and FCA labels page). This rule covers advisers also – the format is non prescriptive.

SDR Labelling – key information

The following is intended to give intermediaries an idea of what SDR labels are and how they operate. This information is not comprehensive. Please see SDR for full information.

Funds must meet specific regulatory requirements in order to use an SDR sustainability label.

The rules are not prescriptive. They intentionally allow for significant strategy variations eg a fund may focus on a single environmental or social issue, or a comprehensive range of sustainability issues.

- Labelled funds must aim to deliver positive environmental and or social (sustainability) outcomes. This may be referred to as ‘intentionality’.

- Only ‘in scope’ funds can opt to use an SDR label.

- SDR does not dictate fund sustainability strategies. A fund may focus on a single environmental or social issue, of a comprehensive range of sustainability issues.

- Processes may be proprietary or aligned to an external service (such as an index) – however in either situation the fund manager is responsible for the strategy.

- Labels are optional. Funds can also be ‘Unlabelled with sustainability characteristics’. Additional disclosures are required for both.

- Labels are not specifically ‘approved’ by the FCA, however amendments to pre-contractual disclosures – typically a fund prospectus – are normally require. Such changes require FCA approval.

- Labelled funds must produce two page client facing disclosure documents (CFD). This is also a requirement for in scope funds that promote sustainability characteristics.

- At least 70% of a labelled fund’s assets must to align to the fund’s objectives – (fund managers must explain how this works in practice).

- No labelled fund assets should conflict with the fund’s sustainability objectives.

- Claims made must be able to be evidenced / proven.

- Labelled strategies must be verified; however this can be done inhouse – subject to the verifier being independent of the specific fund management process – or by a third party.

- Labelled fund stewardship strategies must have escalation plans.

- The four SDR labels have different requirements. These are briefly described below.

Core requirements for all labelled funds:

All funds that chose to adopt an SDR label must publish the following:

- Sustainability objectives

- Documented sustainability policies/strategies

- Sustainability KPIs

- Appropriate resources and governance

- Stewardship strategies

SDR labels – key differences (in our words!)

In scope funds that focus on positive environmental and or social outcomes may choose to use one of the following four labels:

- Sustainability Focus – these funds are required to publish ‘robust evidence-based standards that are an absolute measure of environmental and or social sustainability’.

- Sustainability Improvers –funds that invest in assets that have the potential to improve their environmental and or social standards over time. These will typically lean in to stewardship activity more than funds with other SDR labels. An asset’s path to improvement must be credible. Robust evidence is required.

- Sustainability Impact – this label is for funds with a pre-defined focus on the delivery of positive, measurable environmental and or social impacts. These funds must also have a ‘theory of change’ that describes how the product (eg fund) and, or its assets, will deliver positive impacts, using a robust measurement methodology.

- Sustainability Mixed Goals – for in scope funds that combine two or more of the above approaches.

Also relevant:

- Unlabelled with sustainability characteristics. Funds are not required to adopt a label even if they have a significant focus on sustainability issues – however in scope funds that chose to market their sustainability characteristics without using a label must now adhere to specific rules. Most notably, like labelled funds, they must publish consumer facing disclosure documents (CFDs), and (unlike labelled funds) they are not allowed to use certain terms in their name.

- Other (in scope) funds are only permitted to make ‘short factual statements’ about their sustainability attributes.

- Many funds and products remain our of scope (eg overseas funds and portfolios).

See the FCA’s SDR policy PS23/16 and the FCA’s ESG Handbook for further information and to keep up to date with any possible changes.

Important notes:

- The FCA does not publish a list of labelled funds. Fund EcoMarket carries a list however please be aware this may not be comprehensive (eg some funds to not meet our criteria and some have requested not to be listed at this time).

- SRI Services aims for this information to be up to date and offering a useful overview of the rules for retail intermediaries – however this area has become increasingly complex and rules occasionally change, so please see the FCA’s SDR policy and ESG handbook for full information.

What should advisers and other intermediaries do differently now?

What should advisers and other intermediaries do differently now?

What should advisers and other intermediaries do differently now?Advisers (and other distributors) must make it clear if a fund has a label – by displaying the label – and ensure clients are provided with the relevant CFDs when advising clients on options that are subject to the ‘naming and marketing’ rules.

Advisers must also make it clear that overseas funds are not subject to the UK SDR labelling regime – which is why they are not able to use SDR labels.

Advisers must also provide clients with a link to the FCA’s labelling information page. (Updated February 2026)

How can SRI Services help?

Fund EcoMarket has a filter field that shows individual funds’ SDR labels and status.

Our site has been updated to provide the key information we believe intermediaries are now likely to need.

This includes:

- a filter field that shows individual fund’s SDR status. (This can be used to search or generate lists of funds with specific labels or status).

- additional information within individual fund entries. This includes text and url links to fund manager websites, where Consumer Facing Documents – CFD’s – and other information can be found.

Additional reading / information:

We discussed SDR extensively at our conference on 3 October 2024 and 9 October 2025.

This included presentations from the FCA’s Director of ESG Sacha Sadan and three groups of fund managers exploring different aspects of the new rules in 2025 and the FCA’s technical specialist Louisa Chender presenting in 2025.

See 3 October 2024 SDR presentations and panels discussions here. (These took place when SDR was less than 1 year old.)

See 9 October 2025 SDR presentations and panel discussions here. (These took place when SDR had been live for approaching two years, and labelling became available around 15 months earlier. Individual funds adopted labels at different times, this process remains ongoing.)

We also published a brief introduction to the new rules in January 2024:

Further clarifications were discussed at our 2025 conference by Louisa Chender, who leads much of the FCA’s work in this area:

Fund EcoMarket is free to use thanks to our fund manager partners. (We ask all relevant fund mangers to supply the same information, however partner funds listed first with logos displayed).

Go to the ‘SDR labelling’ filter is in the ‘Fund Basics’ section of the Fund EcoMarket database.

Please do not confuse the SRI Services SRI Styles with SDR (or other) labels …

What makes SRI Styles and SDR labels different?

Our SRI Styles and filters are (very) different from SDR labels, however we believe they compliment the SDR labels.

SRI Styles are based on our judgement, from information published by fund managers. They have no regulatory standing, and are not driven by fund managers, however we believe they compliment SDR as they are more granular and wider in scope than SDR labels. So whilst neither offers a ‘complete picture’ – and therefore should not be used as an indicator of suitability – both can help an intermediary to ‘get started’ in sustainable, responsible and ethical investment. (Our Styles predate the SDR regime by over a decade).

The FCA’s SDR labels aim to help people find in scope funds with aim to deliver positive sustainability outcomes. They are accompanied by a set of rules, as introduced above.

Our SRI styles aim to give a flavour of both the core ‘issue/s’ a fund focuses on (sustainable, environmental, social, ethical, faith) and the funds ‘approach’ taken by the manager ie how/ the way in which issues are integrated into asset selection.

SDR only applies to in scope funds, whereas Fund EcoMarket covers a wider range of funds and products.

Please be aware that this is a fast changing area that continues to evolve.

How do our individual ‘SRI Styles’ relate to the FCA’s SDR labelling regime?

- Sustainability Style – we expect most funds in this style to be broadly in line with the SDR labelling regime – although funds and other options may be ineligible /out of scope or unwilling to adopt labels at this time. These are most likely to be Focus or Impact labels, depending on their strategy.

- Environmental Style – we expect many funds of this kind to be broadly in line with the SDR labelling regime – although funds may be ineligible or unwilling to adopt labels at this time. These are most likely to be Focus or Impact labels, depending on their strategy.

- Social Style – we expect many funds of this kind to be broadly in line with the SDR labelling regime – although funds may be ineligible or unwilling to adopt labels at this time. These are most likely to be Focus or Impact labels, depending on their strategy.

- Ethical Style – we believe many funds of this kind will be suitable for clients with an interest in sustainability however because of the design of the SDR labels most are unlikely to meet the criteria so may opt to be ‘Unlabelled with sustainability characteristics’.

- Faith Style – funds of this kind are unlikely to be aligned to SDR as they do not typically focus on sustainability outcomes.

- Sustainability Tilted funds – some funds in this style may be suited to SDR, although others may not. Some may be suited to the ‘Sustainability Improver’ label if their selection process is designed to them to be overweight in assets that are intentionally transitioning towards higher sustainability standards.

- ESG Plus – some funds of this kind may be suited to SDR, although will may not. For managers who decide to adopt a label the most likely label would be the ‘Improver’ as selection tends to be less strict than some other styles.

- Limited Exclusions – funds of this kind are not likely to align to the SDR labelling regime typically because of their lack of positive focus.

Please note the comments above do not indicate ‘suitability’ – users are recommended to use individual fund and fund manager filters to match client specific aims to fund or product options.

Where can I find further information?

We aim to keep tabs on SDR developments via our blogs, which include both FCA news and our own commentary.

Please be aware – some of this may be superseded or clarified over time.

The most important current links to FCA information are listed below:

- The FCA’s SDR Policy Statement- ( PS23/16: Sustainability Disclosure Requirements (SDR) and investment labels | FCA) – published on 28 November 2023.

- FCA Anti greenwashing rule

- https://www.fca.org.uk/publications/finalised-guidance/fg24-3-finalised-non-handbook-guidance-anti-greenwashing-rule

- https://www.fca.org.uk/publication/finalised-guidance/fg24-3.pdf

- We aim to track these in our blog area, using the ‘SDR’ tag.

- The FCA is publishing additional updates here FCA’s responses to SDR queries

- FCA ESG Handbook ESG Handbook includes more specific information.

- February 2025 update – Handbook Notice 127 here.

- 2024 (some of this is no longer up to date) FCA proposed extending SDR ( anti-greenwash announcement and portfolio consultation) (April 2024)

- Client facing label information on FCA website – to be published by relevant providers/distributors

- Information about the Adviser Sustainability Group

- Pre contractual disclosure FCA guidance

Other relevant compliance links:

- PRIN 2A

- Overseas fund regime update July 2024

- FCA ESG Handbook – (sourcebook updated post SDR) eg:

-

- 5.1, 5.2 & 5.3 Preparation of sustainability disclosures

- 5.4 Labels

- 5.5 Sustainability product reporting

- FCA welcomes ESG ratings and data provider code of conduct December 2023

- FCA Regulatory Initiatives Grid 30 November 2023

- FCA Financial Lives Survey (2022 FLS)