Changes made to Fund EcoMarket SRI Styles classification

Posted on: June 3rd, 2026

Making sustainable and ethical investment look easy

The SRI Services Fund EcoMarket tool helps financial advisers and wealth managers understand sustainable, responsible and ethical investment strategies so that they can be matched to client preferences.

Funds and portfolios are classified into what we call ‘SRI Styles’ to help get people started. There’s no rocket science involved – we simply look at what fund managers say they do in publicly available material – and err on the side of caution if unclear.

We use publicly available information for this so we are looking at same compliance approved information an adviser, portfolio manager or potential client would. Our other information comes directly from fund managers.

We believe looking at published strategy information and information received direct from fund managers is the only sensible way to explore sustainable and ethical investing options. This is because as holdings – or in the case of portfolios – funds – change and opinions vary. So you need to know what their policies say.

This includes looking at stewardship activity. No company is perfect – and issues arise – so it makes the world of difference whether you are, for example, invested via managers who are encouraging greenhouse gas emissions reductions, or only focused on short term returns.

(Please do not confuse our in house classifications with SDR labels or SFDR articles – both have their own filters on Fund EcoMarket.)

Keeping investment classifications up to date

Our challenge since 2011 has been to make that look straightforward (an ongoing battle) – while reflecting ongoing market developments. Strategies and the range of available options shift continually.

This is in part why we regularly review the ‘SRI Styles’ – as we have again recently whilst updating fund and portfolio information.

Alongside fund activity – mergers, SDR labels coming and going, criteria shifting (some up, some down), I found changes in fund management ‘entity’ or ‘company’ level activity interesting.

An important development, that I hope will catch on, is what some are calling ‘baseline policies’ – we call them ‘company wide exclusions’ on Fund EcoMarket).

These used to be rare, but it seems there are now a few fund managers (eg Fidelity, Axa, Aviva, Royal London) who exclude certain areas completely. Examples include; tobacco companies, manufacturers of certain types of armaments (eg chemical weapons), and certain fossil fuels (eg thermal coal), and violators of key international norms (eg UN Global Compact).

Tilting otherwise (what I would call) ‘vanilla’ funds away from such assets is also increasingly popular.

Alongside the shift away from using the word ‘sustainable’ in fund names continues, presumably because of rule changes, there is also a growing range of options with light screens and tilts eg under weighting polluters.

Changes made to our SRI Styles

We have tweaked the name of one of our styles to cover this relatively new and fast growing cohort. These options are, (or will be) listed in the ‘Limited Tilts and Exclusions’ style.

A new ‘style’ for portfolios

A further change we made last week was to add a new ‘Mixed Options’ style. This is for products and services – typically portfolios – that offer more than one strategy option, or bespoke services. We probably should have done that a long time ago!

A good way to help people get started in sustainable investing?

These options won’t suit everyone. I don’t see these strategies competing with funds or entities that only hold assets with high environmental and social standards, that are working to solve problems or have a positive impacts – but they may be a useful entry point for starting to think or talk about these issues. (Does anyone really not care about anything?)

I am also wondering if this might become a transition story. Should any UK investor invest in thermal coal today… particularly if they recognise the chaos climate breakdown will bring – and have made a net zero commitment?

Might such exclusions soon be ‘vanilla’? The new normal?

And might this be a welcome response to the complexity we have tied ourselves up in over recent years? ‘Avoid’, or ‘hold less of’… are both pretty simple, client friendly, messages. Perhaps even helping us to get closer to what research tells us most clients want?

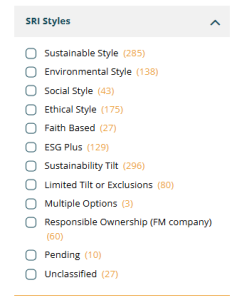

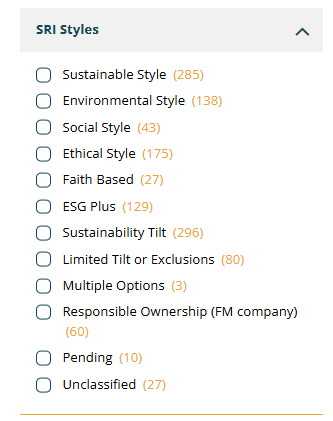

The numbers we display in our styles are at present as follows: