The FCA’s welcome Anti-Greenwash rule is now live – our thoughts

Posted on: May 31st, 2024

SRI Services is delighted to welcome the FCA’s new anti-greenwash rule which takes effect today – and has taken this opportunity to share a few thoughts that may help those effected by the new rule:

We have been seriously concerned about exaggerated and misleading sustainable investment related claims since the area ‘took off’ after the Paris Climate Agreement was signed in 2015 – and have made it clear that we believe this is storing up problems for the future. Risks include not only client disappointment and complaints but also the misallocation of capital and – ultimately – threatening our ability to address climate change and other sustainability challenges.

For the record however, we have never thought that misleading clients was always or necessarily intentional. Indeed, we built a business around helping fund managers to explain what they ‘actually do’ – as all too often people make incorrect assumptions about sustainable, responsible, ESG and ethical characteristics when information is lacking. Most managers gladly share strategy information with us, and we believe this helps reduce related risks.

And we appreciate that the regulator’s interest in this area may not be universally popular as lots of literature and other communications will need to be reviewed. However the FCA’s new greenwash rule is, in our view, simply a clarification of the longstanding ‘clear, fair and not misleading’ rules – which no one now disagrees with – and so should settle down soon. Indeed, recent FCA’s final guidance has helped settle some concerns already. And either way, the anti-greenwash rule is now live, so regulated entities can not ignore it.

The following notes are intended to help those newer to this area. They are not intended to be a comprehensive guide. These are opinions based on experience, and we recommend you read the FCA’s FG24/3 : ‘Finalised non-handbook guidance on the anti-greenwashing rule’ for full information.

These tips focus on retail sustainable investment as that is our area – although the rule applies to all regulated entities. And as with SDR , in order for it to make sense, a good place to start is with its purpose…

These tips focus on retail sustainable investment as that is our area – although the rule applies to all regulated entities. And as with SDR , in order for it to make sense, a good place to start is with its purpose…

- The purpose of anti-greenwash rule. The FCA has always been tasked with helping to protect clients, and amongst other things its remit now also includes the requirement to consider climate change. The anti-greenwash rule is part of a suite of measures that brings these together as there was significant evidence of poor practice. (We define greenwash as ‘exaggerating environmental characteristics for commercial gain’).

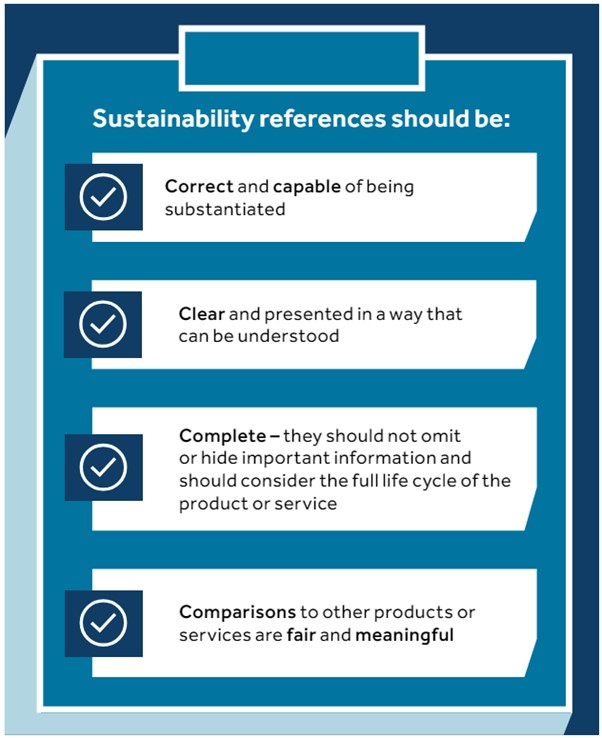

- The FCA’s guidance on anti-greenwash is a starting point not a destination. Context also matters. The new rule is part of a suite of measures announced in SDR. This aspect is born of concerns about clients being misled and trust being eroded – and so was a necessary first step upon which other rules will be built. With regard to what is required, the Final Guidance summary graphic on page 7 is helpful – summarising that ‘sustainability references should be:

- correct and capable of being substantiated

- clear and presented in a way that can be understood

- complete – they should not admit or hide important information and should consider the full life cycle of the product or service

- comparisons to other products or services are fair and meaningful’.

- Not just words. We all know that ‘a pictures speak a thousand words’, so the layout, colours and graphics used by product promoters is important also. The FCA has made it clear that product promoters should not go over the top with this. For example, a dash of green and the odd tree is not a problem – however artwork should be consistent with the strategy that is being described. A fund that largely invests in financials, for example, should not come across as being focused on saving the planet – even if the manager has a clear engagement (stewardship) strategy.

- Be realistic about investee assets. Communications need to be accurate… some companies (and other investee assets) are highly focused on being part of the transition to a sustainable future – whereas others are less so. The difference should be clear to interested clients. However in both instances things can change. Accidents can happen, key people may depart, competitive and external factors may drive changes (eg war, inflation). So implying absolute predictability is not realistic for many assets – particularly where investment selection is driven by historic data. Simple switches such as saying ‘we aim to…’ can help – alongside providing information about what will be done in different scenarios (perhaps via a url link). So from a fund buyer’s perspective, absolute assertions should be regarded as a potential indicator of greenwash.

- Correctly positioning the role of investors. If we are to address issues like climate change, as most people want, investors are going to have to be involved. So offering funds that explicitly aim to deliver positive real world impacts, outcomes and benefits is great. However no single fund or investment house can deliver change on their own – and nor are they directly responsible for delivering change (investors finance change, they don’t make the widgets…), so positioning must be right. Asset managers and others should therefore position the part they play in delivering beneficial and useful products and services carefully. Involvement, influence and agency will vary and should be explained.

- Recognise that sustainability is important and will become more so. The science is clear, climate risk is increasing, as are other sustainability risks. Indeed such risks have the power to ultimately collapse markets and species – including our own. The Institute of Actuaries and others (eg Exeter University) have gone to great lengths explaining this. And of course, alongside risk there are also immense opportunities. Intermediaries, fund pickers, platforms and others should clearly convey both – as their relevance will doubtless increase. Clients may not understand investment well enough to request specific strategies – but people are interested in sustainability and businesses are changing – so learning how to communicate sustainability issues effectively without exaggeration (greenwash) or fear (greenhushing) is increasingly become a core business skill.

- Upskill on sustainability issues. It is not easy communicating sustainability issues to clients (or anyone else). Sustainability, environmental and social issues are realistically something of a labyrinth and to date have largely been outside of many people’s normal work sphere. What’s more, misinformation is rife, opinions vary and things change. The best antidote to this is taking time to understand sustainability issues. The science, the unbiased studies and the opinions of those who use such information in order to try to make the world a better place for others. There are many fantastic sources of information. Some people prefer to go straight to ‘source’ and read information published by the UN (eg IPCC reports), the Met Office and even the World Economic Forum’s risk mapping. A great place to start with understanding where finance collides with sustainability risk is ‘Doughnut Economics’ by economist Kate Raworth. Other books I’d suggest, depending on your interests are scientist Michael Mann’s ‘The New Climate War’, Charles Clover’s ‘Rewilding the Sea’ (an area close to my heart!) and Paul Hawken’s ‘Regeneration, Ending the Climate Crisis in One Generation’.

Further sources:

- https://www.fca.org.uk/publications/finalised-guidance/fg24-3-finalised-non-handbook-guidance-anti-greenwashing-rule

- https://www.fca.org.uk/news/press-releases/sustainability-disclosure-and-labelling-regime-confirmed-fca

- https://www.fundecomarket.co.uk/help/what-is-sdr-article-just-published-in-ilp-moneyfacts/

- https://transitiontaskforce.net/

- https://actuaries.org.uk/news-and-media-releases/news-articles/2023/july/04-july-23-emperor-s-new-climate-scenarios-a-warning-for-financial-services/