Zurich Ninety One Global Environment Pn

SRI Style:

Environmental Style

SDR Labelling:

-

Product:

Pension

Fund Region:

Global

Fund Asset Type:

Equity

Launch Date:

31/07/2006

Last Amended:

Jul 2025

Dialshifter ( ):

):

Fund/Portfolio Size:

£0.04m

(as at: 30/11/2025)

ISIN:

GB00B1746148

Objectives:

The objective of the Strategy is to outperform global equities over the long-term. The Strategy invests primarily in the shares of companies which the Investment Manager believes contribute to positive environmental change through sustainable decarbonisation (the process of reducing carbon dioxide emissions).

Sustainable, Responsible

&/or ESG Overview:

The Global Environment Strategy uses a bespoke bottom-up investment process tailored to a diverse universe of global equities. It incorporates proprietary tools, including our environmental/carbon avoided screen and detailed fundamental financial and risk modelling. We also provide transparency through our annual Impact Report, reflecting our commitment to sustainable long-term investing and active engagement.

We invest in companies positioned to benefit from sustainable decarbonisation. The strategy is a high-conviction, benchmark-agnostic portfolio of best ideas, managed with a long-term horizon of 5–10 years. We focus on holdings that demonstrate:

- Structural growth aligned with decarbonisation

- Sustainable business models and returns

- Competitive advantages over peers

By identifying these traits in each holding, we aim to allocate capital to the leaders of the decarbonisation transition - while avoiding those likely to be left behind. This belief also underpins our conviction in maintaining a concentrated portfolio of industry-leading companies.

Primary fund last amended:

Jul 2025

Information directly from fund manager.

Fund Filters

Sustainability - General

Has policies that consider (environmental and social) sustainability issues. Strategies vary but are likely to consider environmental issues like climate change, carbon emissions, biodiversity loss, resource management, environmental impacts; and social issues like equal opportunities, human rights, labour standards, diversity and adherence to internationally recognised codes. See individual entry information.

Aim to encourage higher sustainability standards through responsible ownership / stewardship / engagement / voting activity

Use the UN Global Compact to inform or help direct where they can or cannot invest. Will typically not invest in companies with significant breaches (low standards) - strategies vary. (The UNGC covers a wide range of issues - search 'UNGC'). See https://unglobalcompact.org/

Publicly report performance against named sustainability objectives

Environmental - General

Has policies which relate to environmental issues. These will typically set out their stance on issues such as pollution, climate change, resource management, biodiversity loss, carbon emissions, plastics and/or additional environmental impacts. Strategies vary.

Options that limit or 'reduce' their exposure to carbon intensive industries (ie sectors which are major contributors to climate change). Strategies vary.

Has a policy or theme that relates to managing natural resources more efficiently. Strategies vary. See individual entry information.

Aims to invest in companies with strong or market leading environmental policies and practices. Strategies vary. See individual entry information for more detail.

Has a written policy or theme focused on waste management - typically to support or encouraging higher levels of recycling and better efficiency / reducing waste. Strategies vary.

Nature & Biodiversity

Has a written biodiversity policy or theme typically aimed at supporting, encouraging and improving environmental protection and safeguarding the natural world (sometimes referred to as 'natural capital'). See eg https://www.un.org/en/climatechange/science/climate-issues/biodiversity

Climate Change & Energy

Has policies (documented strategies that explain their position) on climate change related issues such as greenhouse gas/carbon emissions, net zero, transitioning to lower carbon. Strategies vary.

Avoid investment in major coal, oil and/or gas (extraction) companies. Strategies vary.

Avoid companies involved in fracking and tar sands - which are widely regarded as controversial methods of oil and gas extraction. Strategies vary.

Avoid investing in companies / assets with coal, oil and gas reserves. See individual entry information for further details.

Invest (or may invest) in clean / renewable energy companies and other assets. The proportion directly or indirectly invested in renewable energy may vary over time.

Encourage the transition to lower carbon activities through asset selection and / or responsible ownership activity.

Has an energy efficiency theme - typically meaning that the manager is focused on investing in organisations that manage - or help others to manage - energy use more carefully and less wastefully - and so reduce greenhouse gas emissions.

Invest in renewable energy companies and / or companies where renewable energy is a significant part of their business. Strategies vary.

Has a supply chain decarbonisation policy which sets out their position on the need to reduce carbon emissions.

Has a policy or theme which sets out their position on investment in companies researching/developing hydrogen as an energy solution.

Excludes companies and other assets with direct involvement in fossil fuel exploration (eg coal, oil and gas companies)

Requires all, or most of, the assets they invest in to have a ‘net zero action plan’ - describing how they will reduce their greenhouse gas emissions.

Social / Employment

Aims to invest in assets with high social values - this may include strong human rights, labour standards and equal opportunities or safety related practices.

Has a written diversity policy – where the manager will aim to select companies with a carefully considered, positive employment standards. This may cover a range of issues including gender, ethnicity, disability, beliefs and sexual orientation.

Ethical Values Led Exclusions

Companies are excluded if they are involved in any aspect of the production chain for tobacco products, including cigarettes, vaping, e-cigarettes, chewing tobacco and cigars.

Companies are excluded if they make more than 5% of their revenue from the manufacture, sale or distribution of tobacco products including cigarettes, vaping, e-cigarettes, chewing tobacco and cigars.

Excludes companies which make controversial weapons such as landmines, cluster munitions and chemical weapons.

Avoids companies that manufacture weapons intended specifically for military use. Strategies vary - may or may not include non-strategic military products.

Has a written civilian firearms exclusion policy - meaning that they will not invest in companies that make (or perhaps also sell) handguns made for non-military users.

Gilts & Sovereigns

Does not invest in / excludes 'sovereigns' - debt issued by governments. See eg https://www.investopedia.com/terms/s/sovereign-debt.asp

Governance & Management

Avoids investing in companies with poor governance practices.(e.g. board structure, management practices etc.) Views may however vary on what counts as 'poor' practices - and funds may not immediately divest as they may prefer to work to encourage higher standards.

Exclude companies that are subject to United Nations sanctions. See eg https://main.un.org/securitycouncil/en/content/un-sc-consolidated-list

Encourage the companies they invest in to have more diverse board structures (e.g. more women on boards)

Product / Service Governance

Find fund / asset managers that factor in 'environmental, social and governance' issues as part of their investment decision making process. A focus on 'ESG' typically means a fund is carrying out additional research to help reduce ESG related risks. It does not necessarily mean a focus on sustainability. Strategies vary. See fund literature.

Asset Size

Invests more than half of their money into what are commonly regarded as 'large companies'. This will typically mean that the market capitalisation (or value) of the companies they hold is in excess of £5 to £10 billion.

Invests mainly in larger companies / assets. (e.g. over circa £5-£10bn)

Targeted Positive Investments

Invests >25% of their capital in companies where a major part of their business is focused on helping to address environmental or social challenges.

Invests >50% of their capital in companies where a major part of their business is focused on helping to address environmental or social challenges.

Invests in between 5-25% of capital in assets which meet the EU Taxonomy requirements. This will typically require adding up the proportion of each individual company's activity that is regarded as 'green' so that the manager can produce an overall total for the whole fund or portfolio.

Impact Methodologies

Has policies that aim to help or support the delivery of positive social or environmental impacts (or societal/real world outcomes) by investing in companies they regard as beneficial to people and / or the planet. Strategies vary.

Aims to measure the positive real world environmental and / or social benefits that are associated with their investment strategy. Investments that aim to deliver positive impacts and measure those impacts may be referred to as 'Impact' - although impact measurement is not restricted to Impact investments. Strategies vary.

Investments which are specifically marketed as ‘Impact investments' and work to deliver both financial performance and specific, measurable positive, real world social and/or environmental benefits. Strategies vary.

Specifically sets out to help deliver positive environmental impacts, benefits or 'real world' outcomes.

Directs investment towards companies where a major part of their business is about solving environmental challenges. e.g. companies helping to address climate change.

Specifically sets out to invest in companies that are regarded as 'disrupting' existing business practices - typically through the development of innovative (sustainability aware) products and/or practices.

Aims to deliver positive environmental and or social impacts (real world benefits) through its engagement with investee assets

Invests more than 50% of capital in assets which are regarded as being significantly focused on providing solutions to environmental or social challenges. Strategies vary.

Policy explains the ways in which the manager believes things need to change in order to deliver a more sustainable future, which they are working to help achieve.

How The Fund/Portfolio Works

Focuses on finding and investing in companies with positive / beneficial attributes. This strategy can be applied in addition to exclusion criteria and engagement/stewardship activity.

Has some exclusions - typically for example excludes tobacco or companies that breach commonly adopted standards or norms such as the UN Global Compact.

Publish explanations of their ethical, social and/or environmental policies online (i.e. investment decision making strategies/ buy/sell &/or asset management strategies).

Does not use stock lending for performance or risk purposes.

Unscreened Assets & Cash

Holds between 70-79% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets.

Holds between 80-89% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets.

Holds at least 90% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets.

Intended Clients & Product Options

Designed to meet the needs of individual investors with an interest in sustainability issues.

Designed to meet the needs of individual investors with an interest in ‘Impact investment’ which help or support the delivery of positive social or environmental impacts (or societal/real world outcomes) by investing in companies regarded as beneficial to people and / or the planet. Strategies vary.

Fund Management Company Information

About The Business

Finds fund / asset management companies that have a published company wide stewardship, engagement and / or responsible ownership policy or strategy that covers all investments. Stewardship typically involves encouraging higher ESG standards through voting and dialogue.

Find fund / asset management companies that actively encourage higher 'environmental, social and governance' and / or 'sustainable and responsible investment' practices across investee companies - typically where the aim is to encourage positive change that is aligned with the best interests of investors. Strategies vary. See additional information and options.

Find fund / asset managers that vote all* the shares they own at Annual General Meetings and Extraordinary General Meetings. A commitment to voting shares is a key indicator of 'responsible share ownership' demonstrating their support for or disagreement with management policy. (*situations can legitimately, occasionally occur where voting proves impossible, but in principle all shares should be voted.)

Find fund / asset managers that consider responsible ownership and ESG to be a key differentiator for their business.

The leadership team of this fund / asset manager have performance targets linked to environmental goals.

Find fund / asset management companies that aim to align all their investments (across all funds) to help meet the aims of the UN Sustainable Development Goals.

Find options run by managers that apply Responsible ownership or 'Stewardship' policies to all or most of their investment assets. This means active involvement (e.g. voting, dialogue) with the companies across all or most funds, products and services.

Find fund / asset management companies that consider environmental, social and governance (ESG) issues when deciding whether or not to invest in a company for all / almost all of their funds and other assets. This is increasingly seen as part of sound risk management.

Finds organisations / fund managers that have an in-house (company wide) diversity improvement programme - meaning that they are working to ensure that within their own businesses they employ people from diverse backgrounds - often typically focused on ethnicity and/or sex.

Fund / asset management company has investments in bonds designed to meet sustainability requirements - however these assets may not be 'ringfenced' for this purpose. See website for details.

Fund management entity offers unstructured intermediary training on sustainable investment (ie for financial advisers and wealth managers)

Collaborations & Affiliations

Find fund / asset management companies that have signed up to the UN backed 'Principles of Responsible Investment'.

A member of the Taskforce for Nature Related Financial Disclosures group which aims to aid risk management and shift money towards nature-positive outcomes.

Fund management entity is a member of the Investment Association https://www.theia.org/

Resources

Find fund / asset management companies that employ people to steer and support fund managers in voting shares at company AGM's and EGMs in ways that are consistent with encouraging higher ESG/sustainability standards.

Find a fund / asset management company that directly employs specialist ESG/SRI/sustainability researchers or analysts. This allows asset managers to discuss environmental, social and governance risks and opportunities directly with companies.

Find fund / asset management companies that makes use of expert external research companies. This can help deliver specialist expertise and means resources are pooled with other investors.

Finds organisations / fund managers that have one or more ESG/sustainability experts on all investment teams or 'desks' (all asset types)

Accreditations

Finds organisations / fund managers that have an A+ PRI rating - meaning they are highly rated according to the 'Principles of Responsible Investment'

Find fund / asset managers that are signatories to the FRC UK Stewardship Code, which sets out a framework for constructive investor / investee relations where managers are encouraged to behave like responsible, typically longer term 'company owners'.

Engagement Approach

Find fund / asset management companies that regularly initiate or run industry wide (collaborative) investor projects aimed at raising environmental, social and governance standards amongst investee companies.

Fund / asset manager has stewardship /responsible ownership strategy that is focused on addressing climate change with investee assets.

Fund / asset manager has a stewardship /responsible ownership strategy that involves working with fossil fuel companies on climate change related issues. See fund manager website for details.

Fund / asset manager has stewardship /responsible ownership strategy with involves encouraging investee asset to reduce plastic waste and pollution.

Fund / asset manager has a stewardship / responsible ownership policy that means they are working to encourage more responsible mining practices - where environmental and social issues are properly dealt with by the companies they invest in.

The fund / asset manager has a responsible ownership / stewardship strategy that focuses on biodiversity and nature issues relating to the assets they invest the aim of which will be to reduce harm and or deliver improvement. Strategies vary. https://tnfd.global

Fund / asset manager has a responsible ownership / stewardship strategy which means they are working to encourage the shift to more sustainable business practices in ways that respect and are sensitive to social issues and the impact change has on people effected by the changes that are taking place. https://www.transitionpathwayinitiative.org/ https://transitiontaskforce.net/

Fund / asset manager has responsible ownership / stewardship strategy in place which aims to address human rights issues in investee companies (and potentially their suppliers) with the aim of raising standards

Fund / asset manager has responsible ownership / stewardship strategy in place that aims to improve labour standards for the benefit of employees in investee companies (and potentially their suppliers)

Fund / asset management company has a stewardship strategy in place which involves working to raise diversity, equality and inclusion standards across investee assets

Fund / asset manager is working with the assets they hold to help stamp out modern slavery - where direct or indirect company employees are exploited for business benefits.

Fund / asset managers have stewardship strategies in place that focus on improving governance standards across investee assets

Has a stewardship / responsible ownership strategy that encourages responsible supply chain - ie the managers will discuss environmental, social and governance issues with investee companies with the aim of raising standards

Escalation policies describe how a manager will proceed if stewardship / engagement activity is not successful in the short term.

Company Wide Exclusions

Find fund / asset management companies (not funds) that avoid investment in 'controversial weapons' across all of their funds and other investment vehicles.

Climate & Net Zero Transition

Fund / asset management organisations that have pledged to reduce their greenhouse gas emissions to ‘net zero’. Strategies vary - this area is changing rapidly.

Fund / asset manager AGM / EGM voting strategy has processes in place that mean they will normally be expected to vote in a way that will encourage the transition to net zero greenhouse gas emissions.

This fund / asset management company has set a date by which they plan to achieve net zero greenhouse gas / CO2e emissions.

Find fund / asset management companies that are working with the companies they invest in to encourage reductions in carbon dioxide and other greenhouse gas emissions.

Finds organisations / fund managers that have a company wide carbon transition plan - meaning that they have plotted a path to how they will move away from activities that produce or use carbon based energy sources (that emit greenhouse gases) towards clean, alternative, renewable energy sources.

Finds organisations / fund managers that have published ‘forward looking climate metrics’ e.g. 'implied temperature rise' data that are a total of the asset management company's share (% owned) of all the investee company emissions of the assets they manage, as well as their own direct and other indirect emissions.

This fund / asset management company plans to achieve net zero greenhouse gas (CO2e) emissions with the help of a scheme that will lock away an amount of carbon that is equivalent to the company’s own emissions – so that the end result is ‘net zero’. Calculations and scope vary.

Find fund / asset management companies that are working to reduce their own (fund management company) carbon/greenhouse gas emissions.

Transparency

Find fund / asset management companies that publish a report detailing their responsible investment ownership - also known as 'Stewardship' - activity.

Find fund / asset management companies that publish information about their sustainable and responsible investment strategies on their company website.

This fund / asset management company has published information on their website about the delivery of a 'just transition' - ie the delivery of the necessary shift to a sustainable future that takes full account of social implications - how change effects people. See eg https://www.unepfi.org/social-issues/just-transition/ or LSE Grantham

Fund / asset management companies that publish a full record of how they vote their shares at AGMs (annual general meetings) and EGMs (extraordinary general meetings). Voting strategies have an important role to play encouraging higher environmental, social and governance standards.

This fund / asset management company has published a plan that explains how they are to become a sustainable business - without significant negative environmental or social impacts.

This fund / asset management company has published a plan that explains how they will align to the climate change commitments made at the Paris Climate Talks, COP21.

This fund / asset management company has published a plan that explains how they are going to achieve net zero greenhouse gas / CO2e emissions.

Sustainable, Responsible &/or ESG Policy:

The Global Environment Strategy seeks exposure to themes and companies that will drive the multi-decade process of decarbonisation - the most vital contributor to a sustainable future. To achieve this, we only include companies where we believe the products and services avoid carbon and where we can quantify that carbon is indeed avoided. Our screening process means that to enter the portfolios investment universe a company must have >50% in environmental revenues and quantified carbon avoided, with the environmental revenue classification based on Bloomberg Industry Classification System (BICS). We also exclude any companies with more than 5%* of revenues in Oil, Gas & Coal.

In addition to the universe screen we then carry out detailed fundamental analysis to maintain there is a sound environmental thesis, quantifiable carbon avoided and that the majority of the business is directly linked to the energy transition/sustainable decarbonisation.

More broadly, ESG and sustainability assessments are incorporated into every stage of our investment process, with a focus within fundamental research on understanding the company's management of its positive and negative externalities across natural, social, human and financial capital. Any ESG or sustainability characteristic of a portfolio company that we deem to be sub-optimal or where there is room for improvement, this becomes an engagement goal. We will not invest in any company where we consider there to be material ESG or sustainability concerns, even if the company otherwise meets the criteria of a decarbonisation leader.

* Specifically, we use the following BICs subsectors for this exclusion: Engines & Parts Manufacturing, Exhausts & Emissions Manufacturing, Oil & Gas, Diesel Locomotives Manufacturing, Oil & Gas Infrastructure Construction, Oilfield Chemicals Manufacturing, Coal Mining. This exclusion does not include the Utility sector, which is currently a highly carbon intensive sector but has the greatest potential to ‘avoid’ large amounts of carbon and contribute materially to decarbonisation

We believe there are three compelling reasons to allocate to a portfolio of companies that will enable the process of sustainable decarbonisation, outlined below. Climate strategies vary widely across the peer group. Pure-play renewables and alternative energy funds have struggled in the recent negative beta environment for the theme. By focusing on companies with strong competitive advantages, the Global Environment strategy has better preserved capital than these managers. On the other hand, some climate funds are much more broad, and deliver outcomes more similar to MSCI ACWI. The Global Environment strategy sits between these approaches—more diversified than renewables-focused funds but narrower than broad climate strategies. This balance provides strong exposure to decarbonisation while reducing volatility.

- To gain exposure to a new structural growth area in an otherwise cyclically elevated market backdrop

- Correct the structural underexposure to the enablers and beneficiaries of decarbonisation

- Hedge against systemic carbon risk in portfolios

Achieving such an allocation requires the ability to firstly rigorously screen for and accurately measure the positive carbon impact of a company, before qualitatively appraising its fundamental characteristics. We only include companies in the universe where we are confident that a company plays an important part in offering environmental products and solutions, and where revenues can be directly associated with the concept of ‘carbon avoided’. The Global Environment Strategy employs a bespoke bottom-up investment process designed specifically for this diverse universe of global equities. The process combines proprietary models, such as our environmental/carbon avoided screen, the idea generation ranking process and our detailed company-level fundamental financial and risk modelling, with our qualitative insights, judgments and analysis. We provide transparency on positions and company engagement through our annual Impact Report. This process reflects our core beliefs of sustainable long-term investing and active engagement.

We own companies that we believe will be beneficiaries of sustainable decarbonisation. This is a high conviction concentrated portfolio of best ideas managed to a long-term investment horizon. We seek portfolio holdings that exhibit three characteristics:

- Structural Growth

- Sustainable Returns

- Competitive Advantage

Process:

The Strategy employs a bespoke bottom-up investment process designed specifically for the relevant diverse universe of global equities. The process incorporates proprietary models, such as our environmental/carbon avoided screen and our detailed company-level fundamental financial and risk modelling, but ultimately relies on our qualitative decisions.

Our process has been developed over many years of investing in global equity markets with a focus on environmental/carbon screening, fundamental growth, returns based investment analysis with a focus on sustainability and bottom up stock selection.

The process includes five clear stages:

- Universe Screen

During the initial screening stage, we apply a two-part screening process:

Step one - Environmental Revenues: Initially, we identify those companies that are driving this 'unprecedented shift in energy systems and transport’. It is important to think not just about the direct beneficiaries of decarbonisation, but the entire related supply chain that needs to be built up. The companies which will benefit from the transition to a low carbon economy will likely sit within sectors including industrials, utilities, energy, technology, materials, chemicals and automotive sectors, which represent almost 80% of the GICS.

Our investment framework, created for the transition, encapsulates that there will be winners and losers; for example, as renewable energy grows, fossil electric generation will decline, and we have consequently excluded companies which have revenues that would be significantly eroded by the transition.

Step two – Decarbonisation: Once we’ve found companies that will enable the process of sustainable decarbonisation, we need to determine which companies’ products are genuinely avoiding carbon. We do this through measuring carbon risk and carbon impact as explained below:

- Carbon Risk: While the companies in which we invest are by nature low carbon risk because their business models are highly exposed to sustainable decarbonisation, we believe it’s still very important to monitor and track their carbon footprints. In our view, this means measuring the carbon footprint of every company, including both direct (Scope 1 and 2) and indirect emissions (Scope 3). We work with leading providers of carbon data to estimate all indirect emissions alongside direct emissions where these are not reported by companies, and therefore give a full picture of each company’s carbon footprint including its supply chain and the footprint of the products once they are used.

During this screening stage, we see:

- Scope 1 and 2 carbon footprints as a good proxy for how efficiently the company is managing its business

- The upstream part of Scope 3 acts as a proxy for the efficiency of a company’s supply chain and

- The downstream part of Scope 3 as representative of the efficiency of a company’s products.

- Carbon Impact: To measure this, we use the concept of ‘carbon avoided’. This examines whether the company’s products or services are better in terms of their carbon footprint than the alternative. From here we undergo further analysis to estimate whether the companies in the universe have products and services that avoid carbon. We work with Carbon Disclosure Project to help estimate carbon avoided where it is not reported by companies.

We only include companies in the universe where we believe the products and services avoid carbon and we can quantify that carbon is avoided. The ultimate universe consists of over 1700 companies with a total market cap of US$18 trillion, distributed between the US, China and the rest of the world.

It’s worth noting that our carbon reporting is still at an early stage, much of the data is estimated by our external carbon data provider Urgentem along with CDP and believe that engagement to encourage better reporting is vital to the Strategy. Please see our thought paper: ‘Defining the Global Environment Universe’ for further details.

- Idea Generation

The main source of our idea generation is a screen for companies based on key financial, sustainability and competitive advantage metrics. The metrics chosen derive from decades of investment team and firm-wide experience as well as rigorous back-testing and relevant cross-sector analysis. This screen directs our analyst research which can then lead to further qualitative idea generation.

Given that the universe is rapidly-evolving in a disruptive market, we have analysed several sectors that we believe will share similar characteristics. The key attributes we highlight for relevant cross-sector comparison and analysis include:

- Rapidly improving technology

- Continuously falling costs

- Large capital requirements

This spans many sectors where capital intensity meets technology, with autos, IT and infrastructure/utilities the most relevant. We carried out in depth back-testing on these sectors, and our idea generation screen highlights companies who perform best on metrics most correlated with alpha generation and this is where our analysts focus their attention.

We have also integrated an internal sustainability indicator into this part of the process. This indicator assesses companies across various sustainability and ESG factors that we've identified as being likely to have a financial impact on a company, with each company appraised relative to its sector. Once a company screens to be included in stage 3 (Fundamental Analysis), we perform our own sustainability analysis of the company. This is an integral part of the investment process as we believe that companies with strong sustainability characteristics and who minimise their negative externalities will outperform over time.

- Fundamental Analysis

Companies that look most attractive from our idea generation screen are taken through to the next stage of the investment process where the team conducts the fundamental analysis.

The first stage of our fundamental analysis process is focused on the company’s business model and whether it fits with our requirement for structural growth, sustainable returns and competitive advantage. At this stage we also carry out our own sustainability analysis by assessing the positive and negative externalities generated by the company. When we are comfortable that the company fulfils our requirement and there are no material sustainability risks, we take it forward to a second, more detailed stage of fundamental analysis.

We also conduct detailed fundamental analysis of sub-sectors and technologies exposed to the transition to a low carbon economy. We build sector supply and demand models (e.g., our proprietary global 2 degree model) and undertake thematic research which is presented in our thought pieces “Energy 3.0” which can be found on our website and here. This helps us to inform and stress test our company models.

The key areas of our company research are described below:

Company Analysis

The investment team works through a rigorous checklist for each investment idea. We want to find the best companies in our universe which are intrinsically undervalued. Clean balance sheets and clear business models are a competitive advantage in many parts of this volatile sector.

The team conducts fundamental analysis by constructing detailed models. Our technical understanding and experience looking at these industries, combined with access to the best and most granular data, enables us to construct detailed models that allow us to test different assumptions.

We build an investment case for each idea and focus on the following key factors:

Competitive Advantage

Our competitive advantage analysis can be simplified into the key topics shown below:

- Company factors: Technology, brand, cost competitiveness, R&D spend, and market share

- Market factors: Market growth, pricing power, barriers to entry, substitutes, and consumer acceptance

We use these factors to determine the long-term sustainability of the business in question. In addition, we believe a strong balance sheet and outstanding management are also a competitive advantage and ensure we cover these factors during our fundamental analysis.

Intrinsic Value

The team conducts full financial and valuation analysis by constructing individual company models to determine the growth, earnings and intrinsic value of the companies under review. Our proprietary equity models are maintained within the team and contain our own forecasts. Research from earlier parts of the process is used and built on here. In undertaking full income statement, cashflow statement and balance sheet analysis we can focus on specific financial metrics which we believe to be the drivers of long-term returns. The output of the equity analysis is a target price for the company across different scenarios.

The target price is based on three main components with returns and cash flow being prioritised:

- Free cashflow (DCF)

- Returns analysis (ROCE)

- Multiples analysis (EV/DACF, EV/EBITDA, P/E, P/B)

Return profile and growth

It is important to note that profitable growth and efficient use of capital is embedded within each of the above calculations. Structural growth and sustainable returns are two key drivers of our stock selection and analysis. We believe growth and returns are key factors in determining a reasonable fair value for any company. We therefore do not claim to be only growth or only value investors, instead we invest in the leading companies within our universe that we believe are intrinsically undervalued.

Management, sustainability and engagement

Capital allocation decisions and operational performance are important considerations for us when evaluating management. Much of these considerations feed into our competitive advantage and valuation work. We also place huge significance on sustainability factors as highlighted in our initial screens. Sustainability reports and net zero emissions targets are important throughout our fundamental analysis as well as topics featuring in team debates.

This fundamental bottom-up research stage of the investment process also includes company meetings and onsite visits where we will focus on all the key factors mentioned above. We will only buy a stock for the portfolio after we have met with company management.

When all factors described above score positively for an investment idea, we will add it to our list of best ideas and compare to the existing holdings.

- Portfolio Construction

The best ideas generated through stages 1 – 3 of the investment process are used to construct a portfolio in line with the risk constraints. Ideas are presented in weekly investment meetings and are challenged by the investment team. We operate a team-based approach and all team members have input into idea generation and analysis, with the co-portfolio managers having ultimate decision-making responsibility for the portfolio composition. We will compare any new ideas to the current portfolio characteristics across the main inputs of our investment process.

The portfolio is constructed bottom-up in a benchmark-agnostic fashion. Positions are weighted according to our target prices, strength of competitive advantage and the contribution to the portfolio's risk. The portfolio is then reviewed at a sub-sector level with regards to overall risk budget, sub-sector risks, stress tests and style analytics metrics. Weightings may then be adjusted accordingly. We use MSCI Barra One for quantitative portfolio risk analysis and optimisation.

We will only buy a stock which/when:

- Positively contributes to sustainable decarbonisation

- Exhibits combination of structural growth, sustainable returns and competitive advantage

- Exhibits no material sustainability issues

- Offers upside in company valuation model

- We have met company management

- We have completed our fundamental financial, business and sustainability analysis

- Both co-portfolio managers agree on the investment decision

Sell Discipline

We will revisit a stock if:

- There is a change in structural growth, sustainable returns or competitive advantage or our assessments of externalities

- Share price reaches model target price

- More attractive upside from new ideas

Subsequently, stocks are typically sold when:

- Stock has reached a fair value

- More attractive opportunity has emerged

- Investment case is no longer applicable and reason for investment case revisit hold

- Change in company fundamentals

- Change in regulatory/industry environment

- Adverse change in a company's environmental, social, corporate governance or capital allocation policies

- Engagement and Monitoring

We meet management and engage with all portfolio companies on a regular basis. Topics of engagement are not only on financial and operational issues, but any material sustainability issues. We have ongoing engagement goals for each company and will report on this engagement and progress in our annual impact report. For example, any company that has sustainability characteristics or externalities which are not best in class, automatically becomes an engagement target. We list the engagement targets for each company, along with the reasons why we believe the company fits in the portfolio and the carbon data in our annual impact report.

In our Annual Impact Report, we provide transparency on positions and company engagement, as well as an explanation of why we believe the companies will see structural growth and have a competitive advantage. This report presents significant developments throughout the year, including all environmental metrics for the portfolio and underlying holding as well as engagement goals and progress towards those goals.

We are not naïve on where we can and can’t have influence. There are some engagement goals, for example better carbon disclosure where we would hope to have significant progress in the coming years; others, for example improved gender diversity in the workforce, will regrettably take more time, but we believe are still worth discussing.

Resources, Affiliations & Corporate Strategies:

Ninety One operates a fully integrated approach to ESG, sustainability and stewardship. Therefore sustainability knowledge and expertise is held across a number of areas of the business. The Sustainability Committee oversees the sustainability ecosystem in the business. Ninety One’s firm-wide sustainability strategy and initiatives are overseen by the Chief Sustainability Officer, Nazmeera Moola, supported by the central Sustainability team. This includes investment integration, advocacy, corporate transition to net zero and developing and implementing efforts to mobilise dedicated funding for an inclusive and sustainable transition.

Ultimately, the investment teams have responsibility for managing sustainability risks and opportunities within their investment process through their integration frameworks. We place a big emphasis on ensuring that the investment teams have the appropriate knowledge, insights, data and tools so that the expertise is a truly integrated part of the investment process. The investment teams are supported by dedicated ESG specialists across our Sustainability team and Investment Risk team. We also have further expertise that we can draw upon from the portfolio managers managing our dedicated sustainability strategies, and other sustainability specialists that are dedicated to individual investment teams.

The below provides an overview of the teams, committees and forums with oversight and responsibility for various aspects of sustainability:

Sustainable, Social & Ethics Committee (SS&E)

Oversees compliance with sustainability, social and ethical commitments, targets, and performance.

Reviews sustainability initiatives and implementation across the three pillars of the framework.

Sustainability Committee (SC)

Responsible for the internal oversight of Sustainability and Stewardship, including:

Determining sustainability strategy and monitoring progress on ESG integration, stewardship, advocacy, climate risk, regulation, and other related matters.

Ensuring alignment of focus and integrity throughout the business.

Sustainable Investment Advisory Committee (SIAF)

Responsible for the internal coordination and challenge of investment-related sustainability issues:

Ensuring alignment and compliance of products with sustainability and impact objectives.

Serving as a forum for consultation and discussion on sustainability initiatives, guidelines, and policies.

Sustainability Team

Central custodian of the firm-wide Sustainability strategy, responsible for:

Development of strategy and sustainability and stewardship policies and frameworks.

Promoting best practice ESG integration and stewardship across investment teams.

Coordinating and leading advocacy and firmwide sustainability initiatives.

Providing sustainability expertise and monitoring implementation of sustainability strategy.

Investment Risk Team

Oversight and challenge of firm-wide ESG risk assessment, management, and integration quality.

Management of ESG and climate risk data.

Investment Operations: Proxy Voting

Coordination and execution of the voting process.

Work with the sustainability team to align voting with strategic initiatives.

Investment Teams

Responsible for developing ESG integration frameworks and engagement priorities.

Undertaking ESG analysis, engagement, and voting.

Supporting firmwide initiatives.

Product Development

Manages sustainable product strategy and product development process.

Compliance

Coordinates input on, advises on, and ensures implementation of sustainability-related regulation.

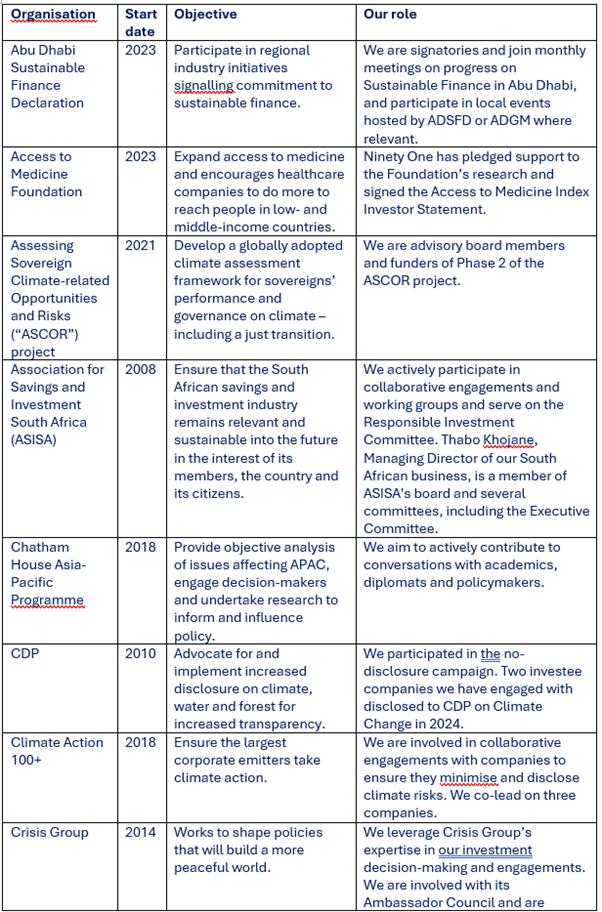

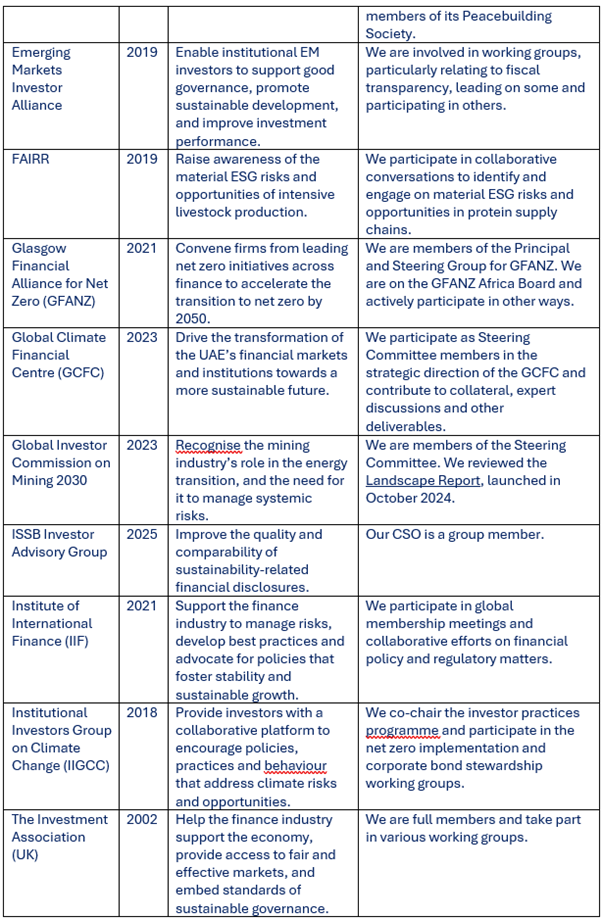

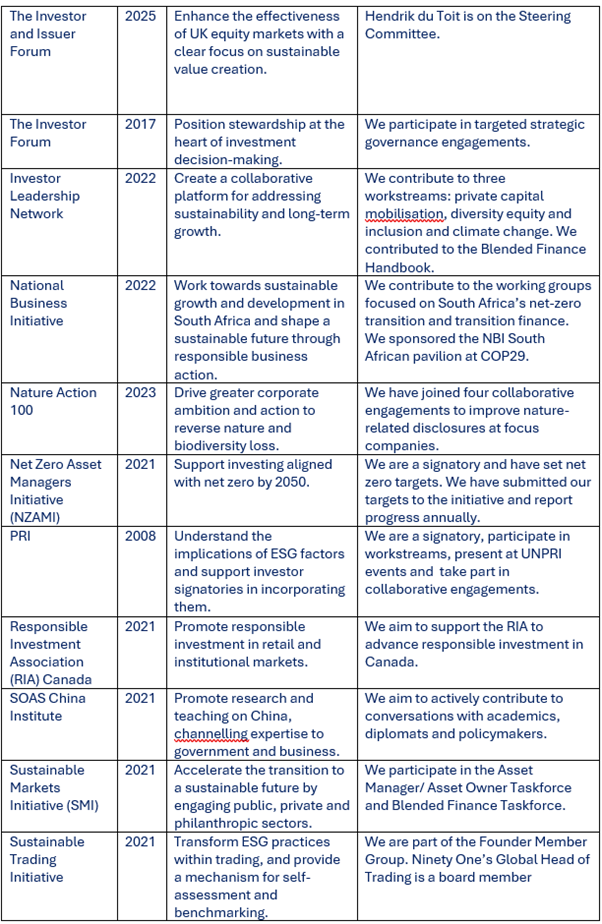

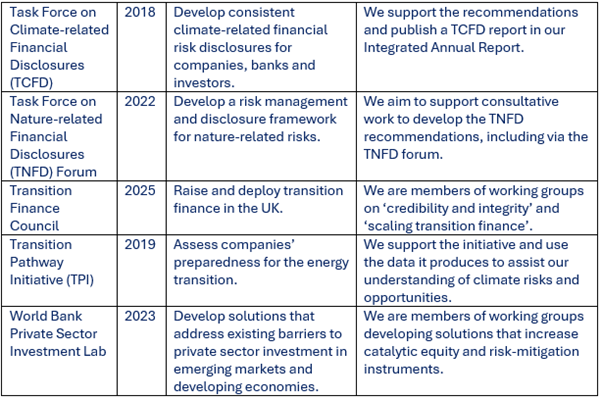

We seek to contribute meaningfully to the conversation on sustainability and to encourage a deeper focus on sustainability-related issues in all of the jurisdictions where we invest, always to the benefit of our clients and their long-term investment outcomes. We may collaborate with other investors as part of an engagement strategy if it can contribute to achieving our engagement objectives and can help address the relevant risks. . Our membership of regional and global organisations facilitates this.

The table below details our firmwide collaborative partnerships and our role:

Literature

Fund Holdings

Voting Record

Disclaimer

Important information

The personal information contained in this document is confidential, and only for the information of the intended recipient.

This communication for professional investors and financial advisors only. It is not to be distributed to retail customers who are resident in countries where the Fund is not registered for sale or in any other circumstances where its distribution is not authorised or is unlawful. Please visit www.ninetyone.com/registrations to check registration by country.

The information may discuss general market activity or industry trends and is not intended to be relied upon as a forecast, research or investment advice. There is no guarantee that views and opinions expressed will be correct. The investment views, analysis and market opinions expressed may not reflect those of Ninety One as a whole, and different views may be expressed based on different investment objectives. Ninety One has prepared this communication based on internally developed data, public and third party sources. Although we believe the information obtained from public and third party sources to be reliable, we have not independently verified it, and we cannot guarantee its accuracy or completeness (ESG-related data is still at an early stage with considerable variation in estimates and disclosure across companies. Double counting is inherent in all aggregate carbon data). Ninety One’s internal data may not be audited. Ninety One does not provide legal or tax advice. Prospective investors should consult their tax advisors before making tax-related investment decisions.

The Funds are sub-fund of the Ninety One Funds Series range (series i - iv) which are incorporated in England and Wales as investment companies with variable capital. Ninety One Fund Managers UK Ltd (registered in England and Wales No. 2392609 and authorised and regulated by the Financial Conduct Authority) is the authorised corporate director of the Ninety One Funds Series range.

This communication is not an invitation to make an investment, nor does it constitute an offer for sale. Any decision to invest in the Fund should be made only after reviewing the full offering documentation, including the Key Investor Information Documents (KIID) and Prospectus, which set out the fund specific risks. Fund prices and copies of the Prospectus, annual and semi-annual Report & Accounts, Instruments of Incorporation and the Key Investor Information Documents may be obtained from www.ninetyone.com.

Daily transactional data is not available to fund investors. Transparency around transactions costs is available to investors via PRIIPs and MiFID methodologies.

THIS INVESTMENT IS NOT FOR SALE TO US PERSONS.

Except as otherwise authorised, this information may not be shown, copied, transmitted, or otherwise given to any third party without Ninety One’s prior written consent. © 2025 Ninety One. All rights reserved. Issued by Ninety One, May 2025.

Indices

Indices are shown for illustrative purposes only, are unmanaged and do not take into account market conditions or the costs associated with investing. Further, the manager’s strategy may deploy investment techniques and instruments not used to generate Index performance. For this reason, the performance of the manager and the Indices are not directly comparable.

If applicable MSCI data is sourced from MSCI Inc. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

If applicable FTSE data is sourced from FTSE International Limited (‘FTSE’) © FTSE 2025. Please note a disclaimer applies to FTSE data and can be found at www.ftse.com/products/downloads/FTSE_Wholly_Owned_Non-Partner.pdf

Targeted or projected performance returns

These are based on Manager’s good faith estimate of the likelihood of the performance of asset classes under current market conditions. There can be no assurances that any investment will generate such returns, that any client or investor will achieve comparable results or that the manager will be able to implement its investment strategy. Actual performance may be adversely affected by a variety of factors, beyond the manager’s control, such as, political, and socio-economic events, adverse changes in the interest rate environment, changes to investment expenses, and a lack of suitable investment opportunities. Accordingly, target returns and expected results may change over time and may differ from previous reports. Additional and supporting information is available upon request.

Hypothetical performance results shown are backtested and do not represent the performance of any account, fund or strategy managed by Ninety One but were achieved by means of the retroactive application, certain aspects of which may have been designed with the benefit of hindsight. The hypothetical back-tested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The actual performance of any account or investment strategy managed by Ninety One will differ, perhaps materially, from the hypothetical back-tested performance results shown herein. Additional and supporting information is available upon request.

This communication includes results which are not historical or actual in nature but are hypothetical illustrations involving modelling components and assumptions that are required for purposes of such hypothetical illustrations. No representations are made as to the accuracy of such hypothetical illustrations or that all assumptions relating to such hypothetical illustrations have been considered or stated or that such hypothetical illustrations will be realized. Actual events are difficult to predict and are beyond the Firm’s control. Actual events may be different, perhaps materially, from those assumed. No investor or client of the Firm has actually experienced the hypothetical results presented. Additional and supporting information is available upon request.

There is no assurance that the persons referenced herein will continue to be involved with investing assets for the Manager, or that other persons not identified herein will become involved at any time without notice. References to specific and periodic team meetings are not guaranteed to be held or fully attended due to reasonable priority driven circumstances and holidays.

Any description or information regarding investment process is provided for illustrative purposes only, may not be fully indicative of any present or future investments and may be changed at the discretion of the manager without notice. References to specific investments, strategies or investment vehicles are for illustrative purposes only and should not be relied upon as a recommendation to purchase or sell such investments or to engage in any particular Strategy. Portfolio data is expected to change and there is no assurance that the actual portfolio will remain as described herein. There is no assurance that the investments presented will be available in the future at the levels presented, with the same characteristics or be available at all. Past performance is no guarantee of future results and has no bearing upon the ability of Manager to construct the illustrative portfolio and implement its investment strategy or investment objective.

References to particular investments or strategies are for illustrative purposes only and should not be seen as a buy, sell or hold recommendation. Such references are not a complete list and other positions, strategies, or vehicles may experience results which differ, perhaps materially, from those presented herein due to different investment objectives, guidelines, or market conditions. The securities or investment products mentioned in this document may not have been registered in any jurisdiction. More information is available upon request.

| Fund Name | SRI Style | SDR Labelling | Product | Region | Asset Type | Launch Date | Last Amended |

|

|---|---|---|---|---|---|---|---|---|

Zurich Ninety One Global Environment Pn |

Environmental Style | - | Pension | Global | Equity | 31/07/2006 | Jul 2025 | |

ObjectivesThe objective of the Strategy is to outperform global equities over the long-term. The Strategy invests primarily in the shares of companies which the Investment Manager believes contribute to positive environmental change through sustainable decarbonisation (the process of reducing carbon dioxide emissions).

|

Fund/Portfolio Size: £0.04m (as at: 30/11/2025) ISIN: GB00B1746148 |

|||||||

Sustainable, Responsible &/or ESG OverviewThis product is linked to the "Ninety One Global Environment" fund. The following information refers to the primary fund. The Global Environment Strategy uses a bespoke bottom-up investment process tailored to a diverse universe of global equities. It incorporates proprietary tools, including our environmental/carbon avoided screen and detailed fundamental financial and risk modelling. We also provide transparency through our annual Impact Report, reflecting our commitment to sustainable long-term investing and active engagement. We invest in companies positioned to benefit from sustainable decarbonisation. The strategy is a high-conviction, benchmark-agnostic portfolio of best ideas, managed with a long-term horizon of 5–10 years. We focus on holdings that demonstrate:

By identifying these traits in each holding, we aim to allocate capital to the leaders of the decarbonisation transition - while avoiding those likely to be left behind. This belief also underpins our conviction in maintaining a concentrated portfolio of industry-leading companies. |

||||||||

|

Primary fund last amended: Jul 2025 |

||||||||

|

Information received directly from Fund Manager |

||||||||

|

Please select what you would like to read:

Fund FiltersSustainability - General

Sustainability policy

Has policies that consider (environmental and social) sustainability issues. Strategies vary but are likely to consider environmental issues like climate change, carbon emissions, biodiversity loss, resource management, environmental impacts; and social issues like equal opportunities, human rights, labour standards, diversity and adherence to internationally recognised codes. See individual entry information.

Encourage more sustainable practices through stewardship

Aim to encourage higher sustainability standards through responsible ownership / stewardship / engagement / voting activity

UN Global Compact linked exclusion policy

Use the UN Global Compact to inform or help direct where they can or cannot invest. Will typically not invest in companies with significant breaches (low standards) - strategies vary. (The UNGC covers a wide range of issues - search 'UNGC'). See https://unglobalcompact.org/

Report against sustainability objectives

Publicly report performance against named sustainability objectives Environmental - General

Environmental policy

Has policies which relate to environmental issues. These will typically set out their stance on issues such as pollution, climate change, resource management, biodiversity loss, carbon emissions, plastics and/or additional environmental impacts. Strategies vary.

Limits exposure to carbon intensive industries

Options that limit or 'reduce' their exposure to carbon intensive industries (ie sectors which are major contributors to climate change). Strategies vary.

Resource efficiency policy or theme

Has a policy or theme that relates to managing natural resources more efficiently. Strategies vary. See individual entry information.

Favours cleaner, greener companies

Aims to invest in companies with strong or market leading environmental policies and practices. Strategies vary. See individual entry information for more detail.

Waste management policy or theme

Has a written policy or theme focused on waste management - typically to support or encouraging higher levels of recycling and better efficiency / reducing waste. Strategies vary. Nature & Biodiversity

Biodiversity / nature policy

Has a written biodiversity policy or theme typically aimed at supporting, encouraging and improving environmental protection and safeguarding the natural world (sometimes referred to as 'natural capital'). See eg https://www.un.org/en/climatechange/science/climate-issues/biodiversity Climate Change & Energy

Climate change / greenhouse gas emissions policy

Has policies (documented strategies that explain their position) on climate change related issues such as greenhouse gas/carbon emissions, net zero, transitioning to lower carbon. Strategies vary.

Coal, oil & / or gas majors excluded

Avoid investment in major coal, oil and/or gas (extraction) companies. Strategies vary.

Fracking & tar sands excluded

Avoid companies involved in fracking and tar sands - which are widely regarded as controversial methods of oil and gas extraction. Strategies vary.

Fossil fuel reserves exclusion

Avoid investing in companies / assets with coal, oil and gas reserves. See individual entry information for further details.

Clean / renewable energy theme or focus

Invest (or may invest) in clean / renewable energy companies and other assets. The proportion directly or indirectly invested in renewable energy may vary over time.

Encourage transition to low carbon through stewardship activity

Encourage the transition to lower carbon activities through asset selection and / or responsible ownership activity.

Energy efficiency theme

Has an energy efficiency theme - typically meaning that the manager is focused on investing in organisations that manage - or help others to manage - energy use more carefully and less wastefully - and so reduce greenhouse gas emissions.

Invests in clean energy / renewables

Invest in renewable energy companies and / or companies where renewable energy is a significant part of their business. Strategies vary.

Supply chain decarbonisation policy

Has a supply chain decarbonisation policy which sets out their position on the need to reduce carbon emissions.

Hydrogen policy or theme

Has a policy or theme which sets out their position on investment in companies researching/developing hydrogen as an energy solution.

Fossil fuel exploration exclusion - direct involvement

Excludes companies and other assets with direct involvement in fossil fuel exploration (eg coal, oil and gas companies)

Require net zero action plan from all / most companies

Requires all, or most of, the assets they invest in to have a ‘net zero action plan’ - describing how they will reduce their greenhouse gas emissions. Social / Employment

Favours companies with strong social policies

Aims to invest in assets with high social values - this may include strong human rights, labour standards and equal opportunities or safety related practices.

Diversity, equality & inclusion Policy (product level)

Has a written diversity policy – where the manager will aim to select companies with a carefully considered, positive employment standards. This may cover a range of issues including gender, ethnicity, disability, beliefs and sexual orientation. Ethical Values Led Exclusions

Tobacco & related product manufacturers excluded

Companies are excluded if they are involved in any aspect of the production chain for tobacco products, including cigarettes, vaping, e-cigarettes, chewing tobacco and cigars.

Tobacco & related products - avoid where revenue > 5%

Companies are excluded if they make more than 5% of their revenue from the manufacture, sale or distribution of tobacco products including cigarettes, vaping, e-cigarettes, chewing tobacco and cigars.

Controversial weapons exclusion

Excludes companies which make controversial weapons such as landmines, cluster munitions and chemical weapons.

Armaments manufacturers avoided

Avoids companies that manufacture weapons intended specifically for military use. Strategies vary - may or may not include non-strategic military products.

Civilian firearms production exclusion

Has a written civilian firearms exclusion policy - meaning that they will not invest in companies that make (or perhaps also sell) handguns made for non-military users. Gilts & Sovereigns

Does not invest in sovereigns

Does not invest in / excludes 'sovereigns' - debt issued by governments. See eg https://www.investopedia.com/terms/s/sovereign-debt.asp Governance & Management

Avoids companies with poor governance

Avoids investing in companies with poor governance practices.(e.g. board structure, management practices etc.) Views may however vary on what counts as 'poor' practices - and funds may not immediately divest as they may prefer to work to encourage higher standards.

UN sanctions exclusion

Exclude companies that are subject to United Nations sanctions. See eg https://main.un.org/securitycouncil/en/content/un-sc-consolidated-list

Encourage board diversity e.g. gender

Encourage the companies they invest in to have more diverse board structures (e.g. more women on boards) Product / Service Governance

ESG integration strategy

Find fund / asset managers that factor in 'environmental, social and governance' issues as part of their investment decision making process. A focus on 'ESG' typically means a fund is carrying out additional research to help reduce ESG related risks. It does not necessarily mean a focus on sustainability. Strategies vary. See fund literature. Asset Size

Over 50% large cap companies

Invests more than half of their money into what are commonly regarded as 'large companies'. This will typically mean that the market capitalisation (or value) of the companies they hold is in excess of £5 to £10 billion.

Invests mostly in large cap companies / assets

Invests mainly in larger companies / assets. (e.g. over circa £5-£10bn) Targeted Positive Investments

Invests >25% in environmental / social solutions companies

Invests >25% of their capital in companies where a major part of their business is focused on helping to address environmental or social challenges.

Invests >50% of fund in environmental / social solutions companies

Invests >50% of their capital in companies where a major part of their business is focused on helping to address environmental or social challenges.

EU Sustainable Finance Taxonomy holdings 5-25% of assets

Invests in between 5-25% of capital in assets which meet the EU Taxonomy requirements. This will typically require adding up the proportion of each individual company's activity that is regarded as 'green' so that the manager can produce an overall total for the whole fund or portfolio. Impact Methodologies

Aims to generate positive impacts (or 'outcomes')

Has policies that aim to help or support the delivery of positive social or environmental impacts (or societal/real world outcomes) by investing in companies they regard as beneficial to people and / or the planet. Strategies vary.

Measures positive impacts

Aims to measure the positive real world environmental and / or social benefits that are associated with their investment strategy. Investments that aim to deliver positive impacts and measure those impacts may be referred to as 'Impact' - although impact measurement is not restricted to Impact investments. Strategies vary.

Described as an ‘impact investment’

Investments which are specifically marketed as ‘Impact investments' and work to deliver both financial performance and specific, measurable positive, real world social and/or environmental benefits. Strategies vary.

Positive environmental impact theme

Specifically sets out to help deliver positive environmental impacts, benefits or 'real world' outcomes.

Invests in environmental solutions companies

Directs investment towards companies where a major part of their business is about solving environmental challenges. e.g. companies helping to address climate change.

Invests in sustainability / ESG disruptors

Specifically sets out to invest in companies that are regarded as 'disrupting' existing business practices - typically through the development of innovative (sustainability aware) products and/or practices.

Aim to deliver positive impacts through engagement

Aims to deliver positive environmental and or social impacts (real world benefits) through its engagement with investee assets

Over 50% in assets providing environmental or social ‘solutions’

Invests more than 50% of capital in assets which are regarded as being significantly focused on providing solutions to environmental or social challenges. Strategies vary.

Publish ‘theory of change’ explanation

Policy explains the ways in which the manager believes things need to change in order to deliver a more sustainable future, which they are working to help achieve. How The Fund/Portfolio Works

Positive selection bias

Focuses on finding and investing in companies with positive / beneficial attributes. This strategy can be applied in addition to exclusion criteria and engagement/stewardship activity.

Limited / few ethical exclusions

Has some exclusions - typically for example excludes tobacco or companies that breach commonly adopted standards or norms such as the UN Global Compact.

SRI / ESG / Ethical policies explained on website

Publish explanations of their ethical, social and/or environmental policies online (i.e. investment decision making strategies/ buy/sell &/or asset management strategies).

Do not use stock / securities lending

Does not use stock lending for performance or risk purposes. Unscreened Assets & Cash

Assets typically aligned to sustainability objectives 70 - 79%

Holds between 70-79% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets.

Assets typically aligned to sustainability objectives 80 – 89%

Holds between 80-89% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets.

Assets typically aligned to sustainability objectives > 90%

Holds at least 90% of assets which align to the sustainability objectives; which are not being held purely for risk management purposes, such as derivatives and cash equivalent assets. Intended Clients & Product Options

Intended for investors interested in sustainability

Designed to meet the needs of individual investors with an interest in sustainability issues.

Intended for clients who want to have a positive impact

Designed to meet the needs of individual investors with an interest in ‘Impact investment’ which help or support the delivery of positive social or environmental impacts (or societal/real world outcomes) by investing in companies regarded as beneficial to people and / or the planet. Strategies vary. Fund Management Company InformationAbout The Business

Responsible ownership / stewardship policy or strategy (AFM company wide)

Finds fund / asset management companies that have a published company wide stewardship, engagement and / or responsible ownership policy or strategy that covers all investments. Stewardship typically involves encouraging higher ESG standards through voting and dialogue.

ESG / SRI engagement (AFM company wide)

Find fund / asset management companies that actively encourage higher 'environmental, social and governance' and / or 'sustainable and responsible investment' practices across investee companies - typically where the aim is to encourage positive change that is aligned with the best interests of investors. Strategies vary. See additional information and options.

Vote all* shares at AGMs / EGMs (AFM company wide)

Find fund / asset managers that vote all* the shares they own at Annual General Meetings and Extraordinary General Meetings. A commitment to voting shares is a key indicator of 'responsible share ownership' demonstrating their support for or disagreement with management policy. (*situations can legitimately, occasionally occur where voting proves impossible, but in principle all shares should be voted.)

Responsible ownership / ESG a key differentiator (AFM company wide)

Find fund / asset managers that consider responsible ownership and ESG to be a key differentiator for their business.

Senior management KPIs include environmental goals (AFM company wide)

The leadership team of this fund / asset manager have performance targets linked to environmental goals.

SDG aligned aims / objectives (AFM company wide)

Find fund / asset management companies that aim to align all their investments (across all funds) to help meet the aims of the UN Sustainable Development Goals.

Responsible ownership policy for non SRI / sustainable funds (AFM company wide)

Find options run by managers that apply Responsible ownership or 'Stewardship' policies to all or most of their investment assets. This means active involvement (e.g. voting, dialogue) with the companies across all or most funds, products and services.

Integrates ESG factors into all / most (AFM) fund research

Find fund / asset management companies that consider environmental, social and governance (ESG) issues when deciding whether or not to invest in a company for all / almost all of their funds and other assets. This is increasingly seen as part of sound risk management.

In-house diversity improvement programme (AFM company wide)

Finds organisations / fund managers that have an in-house (company wide) diversity improvement programme - meaning that they are working to ensure that within their own businesses they employ people from diverse backgrounds - often typically focused on ethnicity and/or sex.

Invests in new sustainability linked bond issuances (AFM company wide)

Fund / asset management company has investments in bonds designed to meet sustainability requirements - however these assets may not be 'ringfenced' for this purpose. See website for details.

Offer structured intermediary training on sustainable investment

Fund management entity offers unstructured intermediary training on sustainable investment (ie for financial advisers and wealth managers) Collaborations & Affiliations

PRI signatory

Find fund / asset management companies that have signed up to the UN backed 'Principles of Responsible Investment'.

TNFD forum member (AFM company wide)

A member of the Taskforce for Nature Related Financial Disclosures group which aims to aid risk management and shift money towards nature-positive outcomes.

Investment Association (IA) member

Fund management entity is a member of the Investment Association https://www.theia.org/ Resources

In-house responsible ownership / voting expertise

Find fund / asset management companies that employ people to steer and support fund managers in voting shares at company AGM's and EGMs in ways that are consistent with encouraging higher ESG/sustainability standards.

Employ specialist ESG / SRI / sustainability researchers

Find a fund / asset management company that directly employs specialist ESG/SRI/sustainability researchers or analysts. This allows asset managers to discuss environmental, social and governance risks and opportunities directly with companies.

Use specialist ESG / SRI / sustainability research companies

Find fund / asset management companies that makes use of expert external research companies. This can help deliver specialist expertise and means resources are pooled with other investors.

ESG specialists on all investment desks (AFM company wide)

Finds organisations / fund managers that have one or more ESG/sustainability experts on all investment teams or 'desks' (all asset types) Accreditations

PRI A+ rated (AFM company wide)

Finds organisations / fund managers that have an A+ PRI rating - meaning they are highly rated according to the 'Principles of Responsible Investment'

UK Stewardship Code signatory (AFM company wide)

Find fund / asset managers that are signatories to the FRC UK Stewardship Code, which sets out a framework for constructive investor / investee relations where managers are encouraged to behave like responsible, typically longer term 'company owners'. Engagement Approach

Regularly lead collaborative ESG initiatives (AFM company wide)

Find fund / asset management companies that regularly initiate or run industry wide (collaborative) investor projects aimed at raising environmental, social and governance standards amongst investee companies.

Engaging on climate change issues

Fund / asset manager has stewardship /responsible ownership strategy that is focused on addressing climate change with investee assets.

Engaging with fossil fuel companies on climate change

Fund / asset manager has a stewardship /responsible ownership strategy that involves working with fossil fuel companies on climate change related issues. See fund manager website for details.

Engaging to reduce plastics pollution / waste

Fund / asset manager has stewardship /responsible ownership strategy with involves encouraging investee asset to reduce plastic waste and pollution.

Engaging to encourage responsible mining practices

Fund / asset manager has a stewardship / responsible ownership policy that means they are working to encourage more responsible mining practices - where environmental and social issues are properly dealt with by the companies they invest in.

Engaging on biodiversity / nature issues

The fund / asset manager has a responsible ownership / stewardship strategy that focuses on biodiversity and nature issues relating to the assets they invest the aim of which will be to reduce harm and or deliver improvement. Strategies vary. https://tnfd.global

Engaging to encourage a Just Transition

Fund / asset manager has a responsible ownership / stewardship strategy which means they are working to encourage the shift to more sustainable business practices in ways that respect and are sensitive to social issues and the impact change has on people effected by the changes that are taking place. https://www.transitionpathwayinitiative.org/ https://transitiontaskforce.net/

Engaging on human rights issues

Fund / asset manager has responsible ownership / stewardship strategy in place which aims to address human rights issues in investee companies (and potentially their suppliers) with the aim of raising standards

Engaging on labour / employment issues

Fund / asset manager has responsible ownership / stewardship strategy in place that aims to improve labour standards for the benefit of employees in investee companies (and potentially their suppliers)

Engaging on diversity, equality & / or inclusion issues

Fund / asset management company has a stewardship strategy in place which involves working to raise diversity, equality and inclusion standards across investee assets

Engaging to stop modern slavery